You can buy cryptocurrency through crypto exchanges, crypto wallets, online exchange services or financial apps that support digital assets. The best option depends on the payment method, available coins, fees, security level and whether you want to store your assets in the same wallet after purchase.

Today, users can buy Bitcoin, Ethereum, USDT, USDC and other cryptocurrencies with a bank card, bank transfer or other available payment methods. For beginners, it is especially important to choose clear services with transparent terms, account protection and the ability to check the final amount before confirming the purchase.

In this article, we will explain where you can buy cryptocurrency, how exchanges, wallets and online exchange services differ, which payment methods may be available and what to check before your first crypto purchase.

Popular Platforms – Exchanges, Instant Exchange Services, and Wallets

Cryptocurrency can be bought in several ways: through crypto exchanges, online exchange services, P2P platforms or crypto wallets with built-in buying and swapping features. Each option has its own advantages: exchanges usually offer a wider choice of assets and higher liquidity, online exchange services make the purchase process simpler, while wallets allow users to store the purchased cryptocurrency in one app.

-

- Cryptocurrency Exchanges. A traditional way to buy crypto by trading on an order book. They offer high liquidity and many tokens, often with the most competitive pricing—but the process can be more complex (deposits/withdrawals, order types) and requires more manual control over fees and settings.

- Online exchange services simplify the buying process: the user selects a cryptocurrency, payment method and sees the estimated or final amount before confirming the transaction. This option can be convenient for quick one-time purchases, but it is important to check the rate, fees, limits, service reputation and conditions for receiving the assets.

- P2P platforms allow users to buy cryptocurrency directly from other users. In this case, the price, payment method and terms depend on a specific offer. P2P can be flexible, but it requires extra caution: users should choose platforms with escrow protection, check the seller’s rating and avoid making payments outside the platform.

- Crypto wallets with built-in buying and exchange features combine several functions in one app: buying cryptocurrency, storing assets, exchanging coins and withdrawing funds. This format is convenient for beginners because there is no need to register separately on an exchange, use a trading terminal or manually move assets between different platforms. Before buying, users should check available coins, fees, payment methods, verification requirements and storage conditions.

Methods of purchase: how they work, with pros & cons

Card (debit/credit; Apple Pay/Google Pay)

The fastest way to get crypto: you pay in EUR and funds are credited almost instantly after 3-D Secure (SCA) approval. This convenience usually means higher processing costs than a bank transfer, and banks may occasionally decline first-time crypto payments.

SEPA bank transfer (EUR)

The most predictable and often the most cost-efficient route for larger deposits. You initiate a transfer to a named IBAN with a unique reference, and the platform credits your balance when the payment lands — typically the same day to 3-4 business days (faster if both banks support instant rails).

Pros: low cost, clear audit trail.

Cons: slower than cards; make sure the sender name matches your account and the reference is exact to avoid delays.

E-wallets

Useful if you prefer not to connect a bank or card directly. Setup is quick and purchases are straightforward, but fees/limits vary by provider and account tier, and sometimes the effective rate is less favorable than SEPA.

P2P marketplaces

You buy from other users using a wide range of payment options. Flexibility is the key advantage, but you take on counterparty risk and must follow platform escrow and KYC rules carefully.

Best for experienced users who understand the trade-offs.

Bitcoin ATMs

Physical machines let you buy with cash or card and receive crypto to your wallet on the spot. They’re fast and convenient, but typically come with the highest spread/fees and daily limits.

How to Choose the Best Option — Comparing Fees and Security

When selecting a platform to buy cryptocurrencies, look past headline exchange rates and consider total cost, security, and ease of use. Differences between services can be significant once you account for deposit/withdrawal fees, card processing costs, spreads, and the time it takes to credit funds.

On traditional exchanges, trading fees are often low, but you may face extra costs for EUR deposits/withdrawals and occasional currency conversion. Processing can also take longer, and the interface requires more hands-on control of order types and settings. Online brokers (instant exchange services) simplify the flow with a single quoted price, but part of the cost is typically built into the exchange-rate margin — you pay for convenience.

From a security standpoint, Trustee Plus applies data encryption, biometric login, and two-factor authentication (2FA). Unlike many exchanges that custody client assets centrally, your funds are held in an individual wallet assigned to you, which reduces single-point-of-failure risk and makes your custody model clearer from day one.

Step-by-Step: Buying Crypto in Trustee Plus

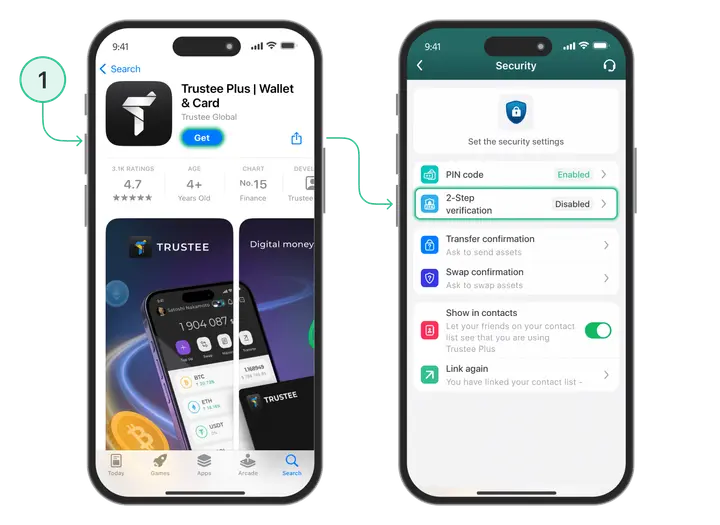

- Install and secure the app.

Download Trustee Plus from your app store, create an account, set a strong passcode or biometrics, and enable 2FA in the Security section. Good device hygiene (OS updates, screen lock) will save you trouble later.

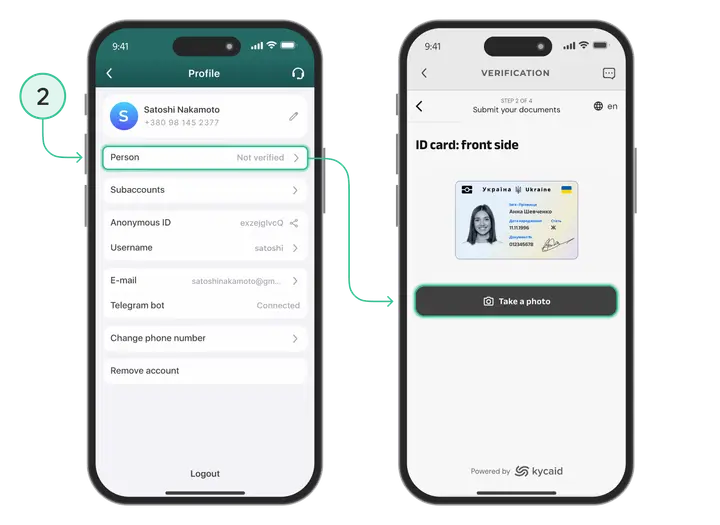

- Verify your identity (KYC).

Start the in-app verification with your ID and a short liveness check. Verification usually completes within minutes, depending on country and provider checks.

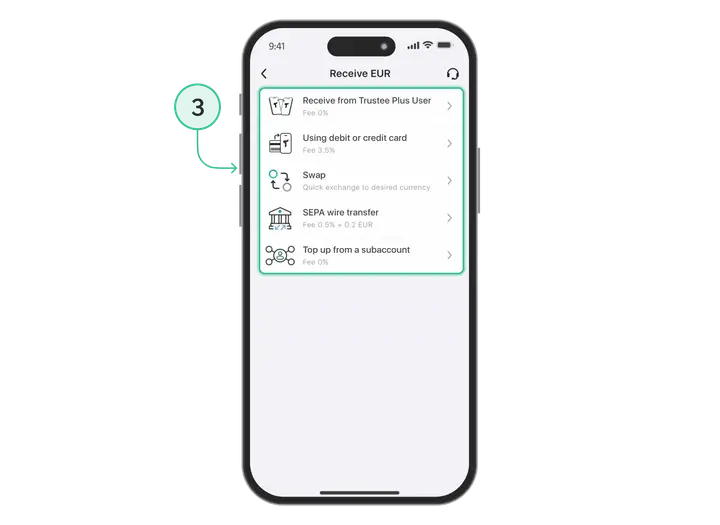

- Top up EUR in the app (Receive → EUR).

On the home screen tap Receive → EUR and add funds:-

Card (euro card): authorize via 3-D Secure/SCA; deposits usually credit near-instantly.

-

SEPA transfer: send from a bank account in your name to the IBAN shown in the app and include your exact payment reference. Arrival is typically same day to 1–2 business days, depending on cut-off times and whether your bank supports instant rails.

-

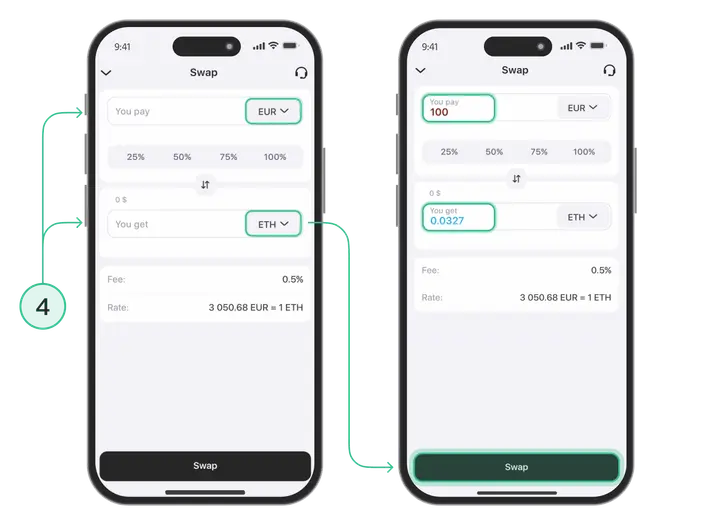

- Once funds are credited and you see your EUR balance, tap SWAP on the home screen.

Set the EUR→crypto pair and review the final quote. In You pay, choose EUR (your in-app balance). In You get, select BTC, ETH, USDC, SOL, or another supported asset and enter the amount. The app shows the final EUR→crypto rate plus the fixed 0.5% service fee (a network fee applies only if you later withdraw on-chain). This is your all-in price—use it to compare with other providers.

- Confirm the swap and receive your crypto.

Tap Swap to convert. Your coins will appear in your in-app wallet. You can also export a receipt for your records or accounting.

How to secure funds and avoid fraud

Right after purchase, choose where you’ll keep assets: custodial (Trustee Plus) or non-custodial (Trustee Wallet).

In a custodial setup, harden your account first: enable 2FA and biometrics, use a unique strong password, and (where available) turn on withdrawal allowlists/alerts. Access the app/website only from your own bookmarks and verify the publisher before installing updates. For cards, be ready for 3-D Secure; for SEPA, ensure the sender name matches your profile and include the exact payment reference. For larger, long-term holdings, consider periodically moving a portion to self-custody.

In a non-custodial setup, your recovery phrase is the master key. Write it down offline, store it in two secure places, and never type it into any website, chat, or “support” form. Keep your phone OS and the app updated, use biometrics/screen lock, and (advanced) consider an extra passphrase. Test a small restore on a spare device or hardware wallet before moving significant value.

Stay alert to phishing/social engineering: start from your bookmarks, check domains, ignore unsolicited links. No legitimate support will ask for your recovery phrase or remote access. When sending funds, do a small test, confirm the network/address format. For P2P, keep communication on-platform, use escrow, and choose well-rated counterparties.

Summary

Buying crypto in Europe is straightforward — pick the channel that fits your priority: speed (cards), total cost on larger amounts (SEPA), or simplicity (online brokers and wallets with built-in exchange). Exchanges still rule for active trading and market depth, while brokers trade price for convenience.

Trustee Plus is one example of this approach: the app allows users to buy, store and exchange cryptocurrency in one place. However, before buying any asset, users should independently check the transaction terms, fees and possible risks.